Freelancing in Portugal usually means you’re taxed through three separate systems:

- IRS (income tax) — what you pay on your annual profit/income

- Social Security (Segurança Social) — contributions based on reported activity income

- VAT (IVA) — whether you must add VAT to invoices, and whether you can reclaim VAT on costs

You will very likely not have any surprises if you understand these three.

Your goal as a freelancer should be to structure things so you pay no more than required while keeping your cash flow requirements predictable.

1) IRS

Most freelancers are taxed under the Category B of the IRS (self-employment).

But how your taxable income is calculated depends on:

- Your CAE / business category which you have set out in the tax authority website

- The accounting regime you are under to determine your taxable income

For the accounting regimes, you may be using:

Option A: Simplified regime

Under the simplified regime, taxable income is not based on your real expenses. Instead, the tax authority applies a coefficient to your revenue.

For many service activities, a 0.75 coefficient is commonly applied (meaning only 75% of revenue is treated as taxable income).

Many professional service activities do not have expenses that reach 25% of revenue, which is why the simplified regime can be efficient when real costs are low.

Important:

Even in the simplified regime, there are cases where you need to “justify” part of that presumed expense component through properly issued invoices and expense allocation (often through E-Fatura classification).

Option B: Organized accounting

Here, you are taxed on real profit:

Revenue – allowable expenses = taxable profit

There is more administrative work under this regime but can become more tax-efficient when your costs are meaningfully higher relative to revenue (or when your activity becomes more complex).

2) Social Security

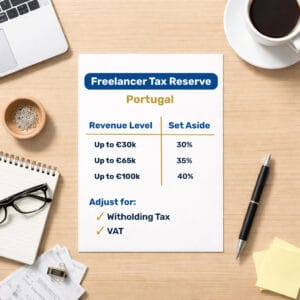

Freelancers generally pay Social Security contributions using a rate of 21.4% applied to a calculated contribution base (70% of income for most freelancers) and payable monthly.

Note that freelancers do not pay any Social Security contributions in their first 12 months of activity.

As such, this becomes a meaningful cost after the first year of activity because:

- It is separate from IRS and becomes a new tax you must pay

- It will undoubtedly affect monthly cash flow

- It becomes very noticeable once income rises

Important:

Many freelancers plan only for IRS and then get caught by Social Security outflows.

You should treat Social Security as a fixed monthly cost of operating after your first year of activity and provision for it monthly.

3) VAT: Do you need to charge it?

VAT is a transaction tax you collect and pay to the State.

You may be exempt from colecting VAT depending on your activity.

However, many freelancers are exempt because their expected turnover is below the threshold associated with the special small business exemption regime (a turnover below €15,000 in a calendar year).

Freelancers may still lose the exemption during the year.

If you benefit from the VAT exemption:

- You usually do not charge VAT to clients

- You generally have less VAT reporting

- But you also typically cannot recover VAT on your business costs (which matters if you have meaningful VAT-deductible expenses)

If you need to charge VAT:

- You must charge VAT on your services and remit it to the State

- You are required to file periodic VAT returns (monthly or quarterly)

- You can recover VAT on eligible business expenses

- You need to manage cash flow carefully, as collected VAT is not your income

The 6 decisions that drive your net outcome

If you want a simple way to think about “tax efficiency” as a freelancer, these are the levers that matter most:

1) Are you in the right IRS regime?

Simplified can be efficient; organized can be better once costs rise or when the complexity of your business increases.

Practical check:

Review your tax regime to determine which is the most efficient for your business. If you do nothing, you can stay in an inefficient structure for years paying way more tax than you should.

2) Is your activity correctly registered in the tax authority website?

This drives what rules tend to apply and what assumptions you may be taxed under when you are under the simplified accouting regime.

This is one of the first things that must be addressed after opening activity.

Practical check:

Confirm whether your activity code is appropriately set out in the tax authority website. This can have a massive impact on your tax bill.

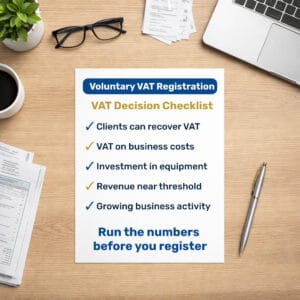

3) Should you remain VAT-exempt or enter the normal VAT regime?

If your clients are businesses that reclaim VAT, charging VAT may not hurt competitiveness.

If you have meaningful VAT on costs (equipment, software, rent), the ability to reclaim can matter.

The correct answer depends on client profile and cost structure.

Practical check:

Confirm your VAT status: exempt or in the normal VAT regime.

Do not be the freelancer that does not understand VAT exemption limitations until a client asks for a VAT invoice or you receive an email from the tax authority.

4) Are your costs being captured properly (even in the simplified regime)?

Even under simplified, treatment/recognition of expenses and correct allocation in the system can affect what is accepted as a deductible business expense.

Practical check:

Ensure your invoicing and expenses are properly documented.

Leaving invoice organisation to the end of the year usually creates avoidable tax and stress.

5) Are you provisioning for IRS and Social Security?

Do not treat taxes as surprises to be unrapped whenever you receive a tax bill. The correct approach is to set aside an expected tax amount monthly.

Practical check:

Set a routine for monthly provisioning for IRS and Social Security – do not treat taxes as an afterthought.

6) Is your structure still appropriate as income grows?

At some point, you may need to reassess whether your business structure is still efficient:

- simplified vs organized accounting

- VAT status

- whether you should remain as a sole trader or consider incorporation

Practical check:

Reassess your structure when revenue or costs change materially (don’t wait for a surpise letter or email revealing a problem).

Retenção na Fonte (Tax Withholding)

In some cases, part of your invoice is withheld by your client and paid directly to the tax authority. This is called tax withholding.

This is not an extra tax. It is simply an advance payment of your IRS — so it has no impact on your annual net income.

At the end of the year, the tax withheld during the year is deducted from your final IRS calculation. If too much was withheld, you receive a refund. If too little was withheld, you pay the difference.

For many professional services, the withholding rate is 23% of the invoice value (excluding VAT) when invoicing businesses.

However, freelancers with annual revenue below €15,000 may choose not to apply withholding tax requirements.

In this case, you will receive the full invoice amount, but you must still ensure that you set aside money to pay your tax bill at the year-end – since nothing has been prepaid during the year.

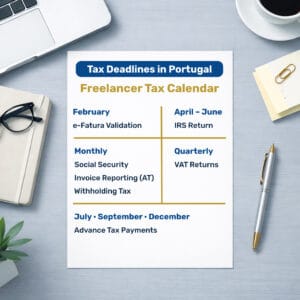

Pagamentos por Conta (Advance Tax Payments)

After two calendar years of freelancing, the tax authority may require advance tax payments.

Like withholding tax, these payments are not an additional tax. These are advance payments of IRS made during the year, based on the tax calculated from your previous tax returns.

They are typically paid in three instalments during the year (July, September and December).

When the final IRS is assessed, the advance tax payments already paid are deducted. If the advance payments exceed the final tax due, the difference is refunded. If they are lower, the remaining balance must be paid.

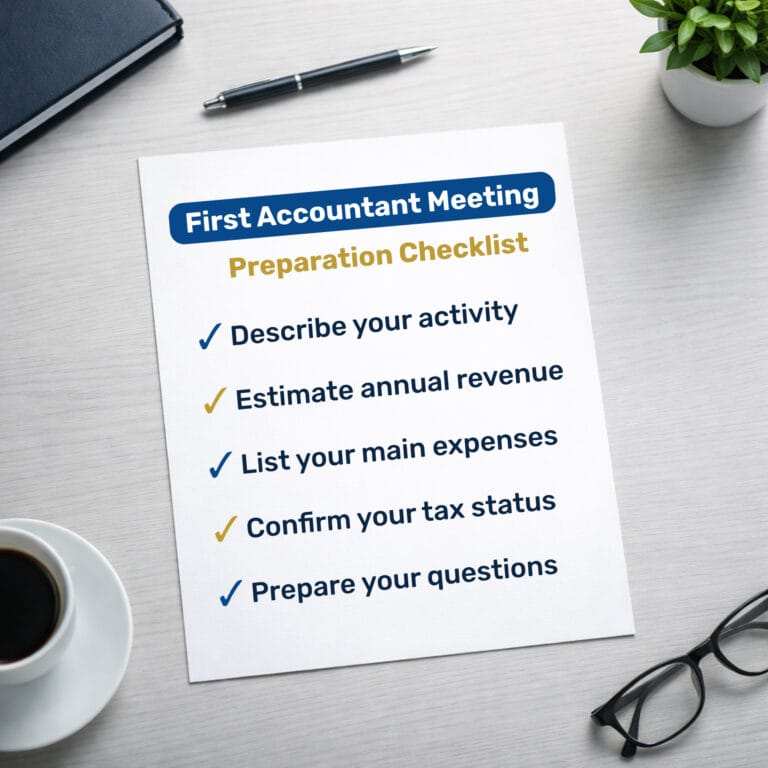

When an accountant becomes “worth it” for freelancers

An accountant is most valuable when they prevent expensive decisions — not when they file forms.

Ask your accountant for a proper review when:

- your revenue is increasing

- you are worried that your VAT status may change

- you are unsure whether simplified is still efficient

- you are starting to subcontract/hire

- you want cashflow predictability