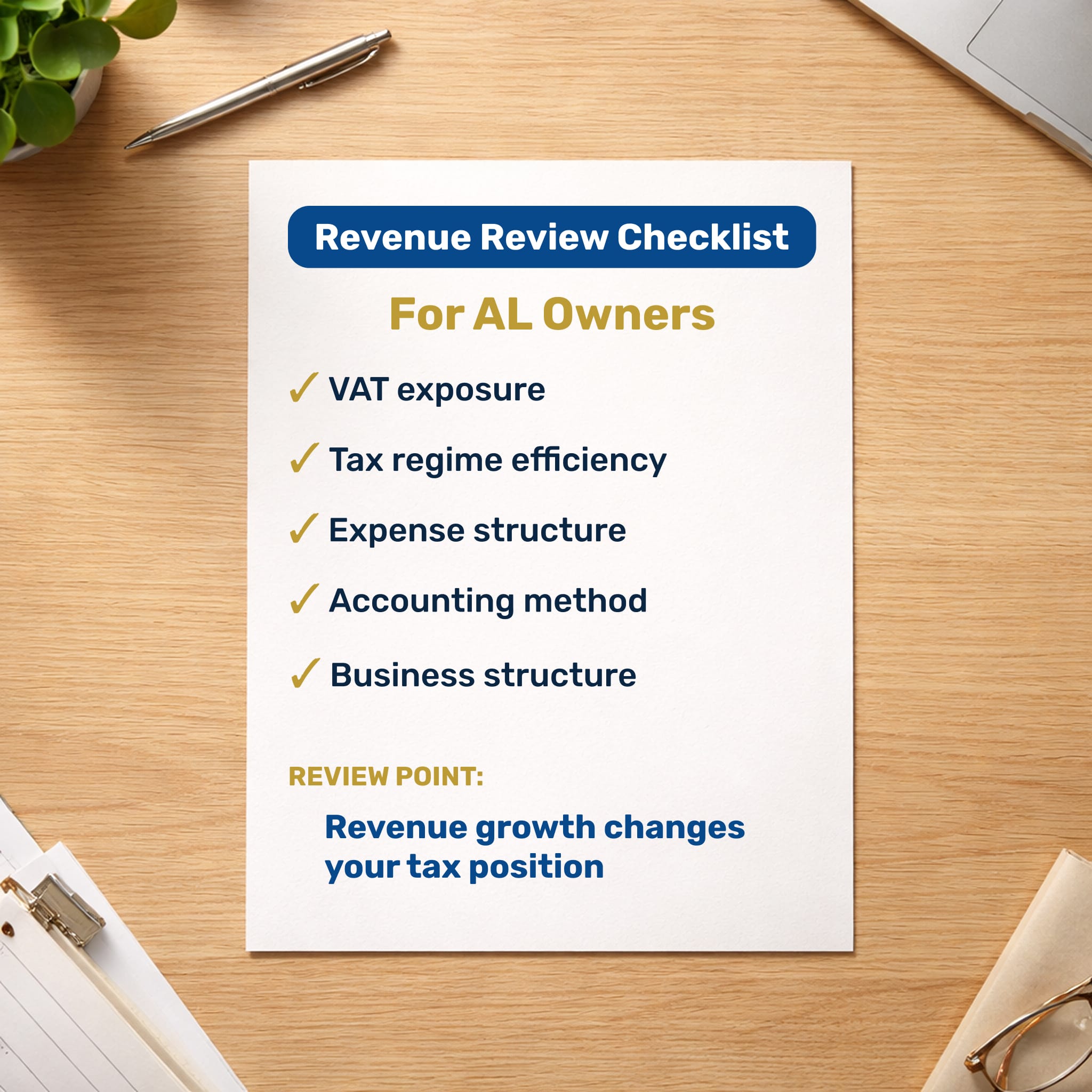

When you run a short-term rental (AL) in Portugal, revenue growth is always good — but it often comes with new rules, new exposure, and (sometimes) opportunities to structure things better.

Once you cross certain thresholds, you should expect changes in VAT, tax regime efficiency, compliance risk.

This article is a practical checklist of what to review as your AL income grows.

What Typically Changes as Revenue Grows

1) VAT enters the equation

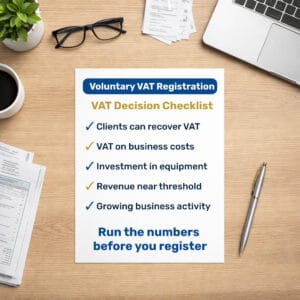

Many owners start with not charging VAT but once revenue rises, you should review:

- whether you are required to register for VAT

- whether you should voluntarily register (sometimes beneficial)

Why this matters:

- VAT registration can change your pricing strategy (do you raise prices or absorb VAT?)

- it can improve tax efficiency if you have meaningful VAT on costs (renovations, furniture, management services), depending on your situation

- it increases reporting obligations and penalty exposure if mishandled

The more your revenue increases, the less you can afford “guesswork” on VAT.

2) The simplified regime can stop being efficient

Many short-term rental owners are taxed under the simplified regime, where the tax authority assumes a fixed percentage of revenue represents expenses.

This often works well when turnover is relatively low. However, as revenue increases, this assumption may no longer reflect how your business actually operates.

Once revenue grows, two situations typically arise.

Scenario A: your real costs are relatively low

If the property generates revenue with limited ongoing costs:

- the simplified regime may still remain efficient

- the administrative simplicity can be valuable

But you should confirm your effective tax rate is still reasonable. Marginal tax rates on higher income brackets can reach up to 48%.

Scenario B: your real costs are significant

In other cases, the cost structure is much heavier than the simplified regime assumes. You could have:

- upcoming renovations

- large furniture/maintenance spending

- cleaning and laundry fees

- management commissions

- mortgages (note: not always deductible depending on structure)

- utilities and insurance costs

- platform fees (Airbnb, Booking, etc.)

If your real costs are significant, being taxed by the tax authority on an “assumed profit” can mean paying tax on income you didn’t actually keep.

What to do:

At higher revenue levels, you should run the numbers and compare:

- the assumed taxable profit under the simplified regime, and

- taxable profit based on actual costs

Note that even small percentage differences become meaningful when your revenue is higher.

3) Compliance risk increases (and the cost of mistakes rises)

At low levels of activity, mistakes often go unnoticed. At higher revenue, you tend to have:

- more transactions

- more reporting trails (more platforms used, transactions, etc.)

- more banking movement

- more third-party visibility

With this extra exposure problems usually appear such as:

- incorrect invoicing (or gaps in invoicing)

- mismatches between platform income and declared income

- missing or incorrect VAT handling (if applicable)

- poor documentation for expenses

- misunderstanding what is “personal” vs “business” spending

At low levels of activity, small administrative gaps may go unnoticed. As revenue increases, the volume of transactions creates a clearer trail, and inconsistencies become easier to detect.

4) Structure decisions become worth revisiting

A company is not automatically better. But at certain revenue levels, it becomes worth reviewing because:

- your IRS marginal rates may be high enough that alternative structures can improve net income

- you may want clearer separation of personal and business finances

- you may plan to scale (multiple units, staff, management team)

- you may want to reinvest profits rather than withdraw everything (which may lead to more tax even if you reinvest later)

Important

Incorporating without a plan often creates more complexity without improving tax outcome.

The right approach is to review it when:

- profits become consistently meaningful

- you want to reinvest

- you’re paying a high effective tax rate

- you want operational and risk separation

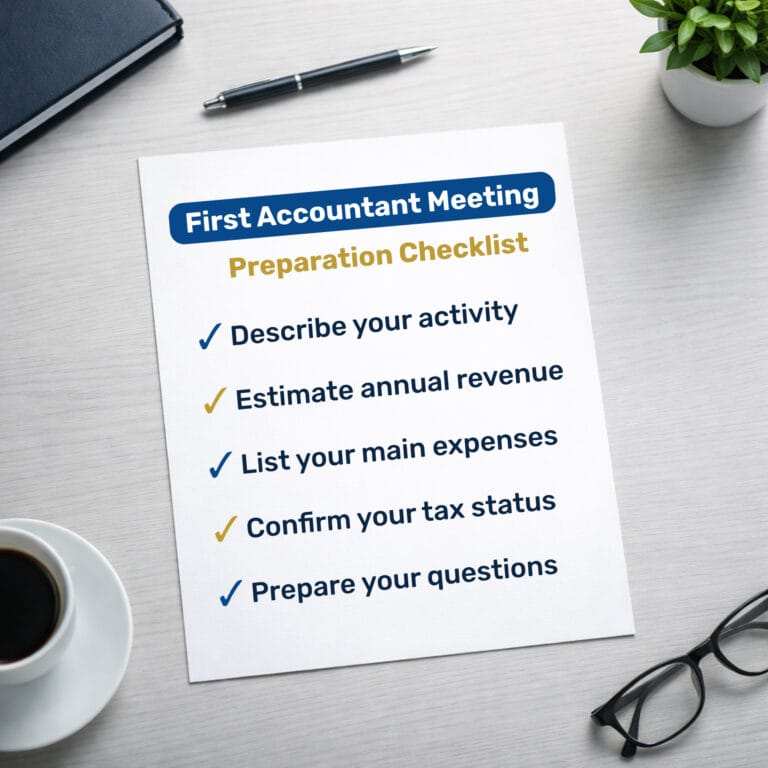

A Simple Checklist

You should schedule a proper review with an accountant if any of these is true:

- Your revenue has increased materially year-on-year

- You added a second unit (or plan to)

- Cleaning/management/maintenance costs are now a major cost

- You’re spending significant money on upgrades

- You’re unsure whether VAT applies to your situation

- You want to reinvest rather than withdraw all profits personally

This review should be numerical and practical.

What to Track Monthly So You Can Make Better Decisions

Every month, as bare minimum track:

- total platform revenue (gross — not the credit in your bank account)

- platform fees

- cleaning / laundry

- maintenance

- utilities

- management commissions

- other recurring costs

- one-off spending (renovations, furniture)

Why this matters:

- It lets you quickly see if your real cost structure is close to (or above) what the “simplified assumptions” treat as expenses

- It makes regime comparisons straightforward

Common Misconceptions

- “If I register for VAT, I’ll automatically pay more tax.”

- Not always. VAT affects pricing and compliance, but input VAT may be relevant in some situations.

- “A company is always better once revenue is high.”

- Not always. It depends on profit level, withdrawal strategy, and reinvestment plans.

- “Accounting fees are the main cost of changing structure.”

- Usually false. The main cost is choosing the wrong structure and paying unnecessary tax.

Final thought

At a small scale, a simple tax structure is often the answer.

If your revenue has recently increased, it might be a good time consider whether you are paying tax based on how my business actually works.

No one wants to pay tax based on assumptions made by the tax authority that reduce their take-home pay.