The simplified regime is very popular for one reason: it’s easy.

However, as your revenue grows, you may be willing to sacrifice simplicity for a more efficient tax regime.

If your activity has grown, or your costs have changed, the simplified regime can become very expensive. This article shows you how to check whether this regime is still working for you.

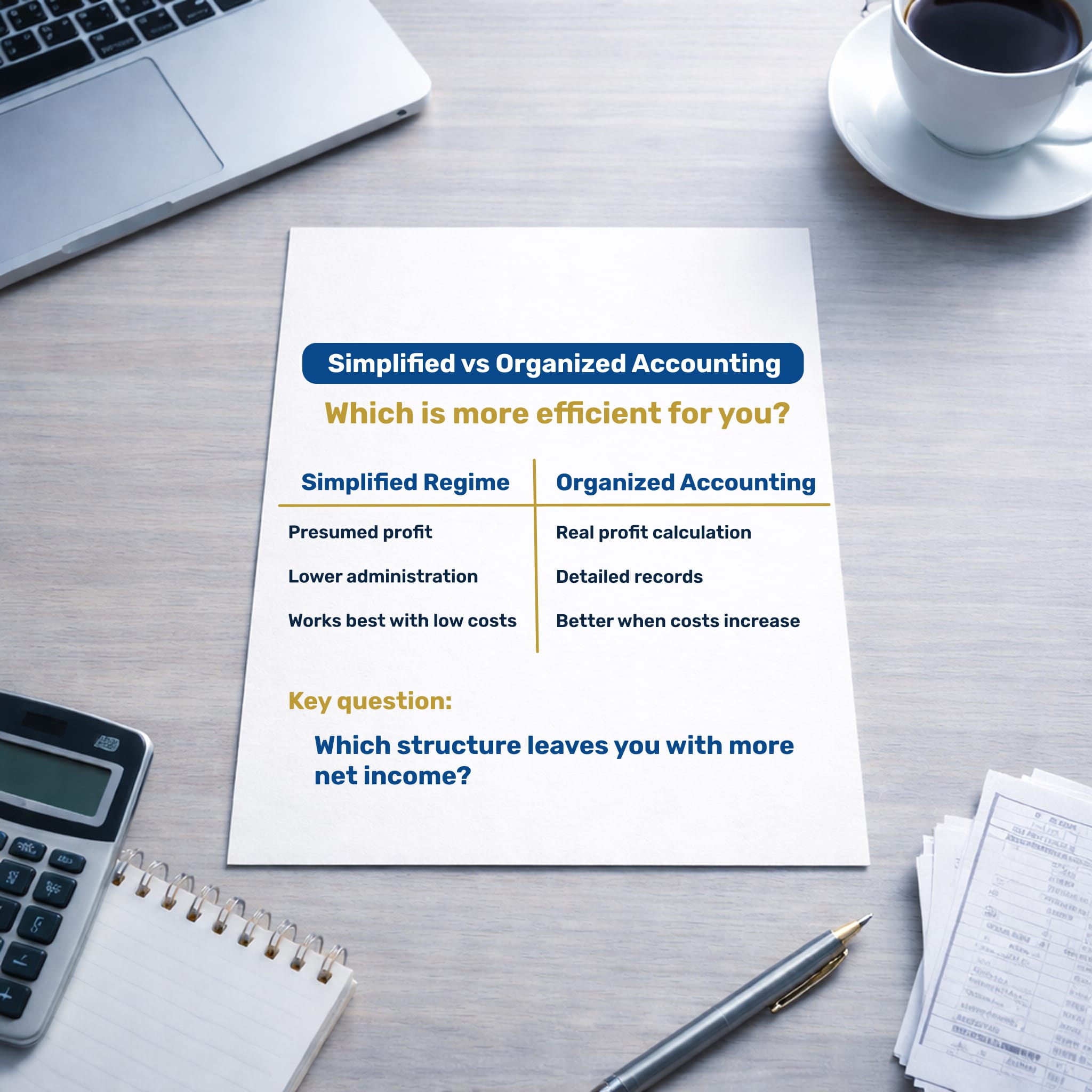

Understanding the simplified regime

Under the simplified regime, you are not taxed on your real profit.

You are taxed on a presumed profit calculated using a coefficient (a fixed percentage of your revenue).

For most service activities, the system assumes your business costs are 25% of your total revenue — even if your real costs are higher.

That assumption can be fair at the start. It can become unfair later.

Do this simple self-check

Take the last 6 months and write down:

- Total revenue (your invoices)

- Total business costs that are actually business related (shown in the supplier’s invoices/receipts)

Now calculate:

Your real cost percentage = Real costs / Revenue

Then compare that number to the simplified regime’s assumed costs for your activity. For most service businesses, the regime assumes costs equal to 25% of revenue, while for short-term rental activity the assumed costs are 65% of revenue.

If your real costs are higher than what simplified assumes, organized accounting often becomes more efficient.

When simplified often stops being efficient

You should review your regime if any of these are true:

1) Your costs are no longer light

Common cost increases:

- renting an office or workspace

- subcontracting work

- hiring someone

- having significant software/tools/licenses

- traveling often for work

- buying equipment (and keep investing)

If your real costs are now meaningful, simplified can tax you on profit you did not actually keep.

2) Your revenue has increased

When income rises, small percentage differences become large tax differences. Especially because marginal tax rates in Portugal can go up to 48%.

Example logic:

- At €20k in revenue, an additional 2% effective tax rate costs €400, so you may tolerate some inefficiency.

- At €80k in revenue, the same 2% costs €1,600, which makes optimisation more worthwhile.

As your activity grows, it becomes important to reassess whether your current setup is still the most efficient.

3) Your activity is not just about you anymore

Simplified tends to fit low-cost, solo, service-based work.

It tends to fit less well when:

- you are building an operation composed of various individuals

- you depend on suppliers/subcontractors

- you have recurring operational costs

- you want clearer financial reporting to help with financing

4) You feel “tax surprised” every year

A common signal is when the numbers start to feel disconnected “weird”.

This happens when your operating costs have increased or your margins are not particularly high, yet you feel your taxable income and/or tax bill remains relatively large.

That’s often a sign you are taxed on a presumed profit which no longer matches the reality of your business.

A simple example

Assume your activity is taxed under simplified as if 75% of revenue is taxable (typical for many service activities).

Scenario A — Simplified still works

- Revenue: €50,000

- Real costs: €8,000 (16%)

- Simplified assumes costs: €12,500 (25%)

Here, simplified is efficient.

Scenario B — Simplified becomes expensive

- Revenue: €50,000

- Real costs: €18,000 (36%)

- Simplified assumes costs: €12,500 (25%)

In this case, simplified taxes you as if you kept more profit than you actually did. That difference is taxed at your IRS rates — and the impact grows quickly.

Accounting fees rarely cancel the benefit of organized accounting

A common hesitation when considering organized accounting is the cost of hiring an accountant, which is required under this regime.

However, this is often the wrong comparison. What should be asked is:

Do the tax savings exceed the cost of hiring an accountant?

If your real business expenses are meaningfully higher than the assumptions used in the simplified regime, organized accounting allows those costs to be fully recognised.

In practice, the difference in taxable income can often be larger than the difference in accounting fees.

This decision should always be reviewed numerically.

When the Simplified Regime Is No Longer Efficient

The usual paths are:

Option 1 — Move to organized accounting

Best when you have:

- consistent real costs

- subcontractors or employees

- significant running costs

- a need for more detailed reporting

Option 2 — Consider incorporation

Not always optimal, but worth reviewing when:

- profits are high

- you plan to reinvest

- you require liability protection

- you want greater planning flexibility

Again, This decision should be based on a numerical analysis.

Final Thoughts

The simplified regime is a good default — until your business stops being “simple”.

A practical review once a year can prevent you from being taxed on profit you didn’t actually keep.

Efficiency is about paying the right tax based on how your business actually works.