VAT is important because it affects your pricing, your margins, your reporting obligations, and how your activity scales.

You need to charge VAT when you are in the normal VAT regime and the service you provide is taxable in Portugal.

If you are covered by a VAT exemption, you generally do not charge VAT — but you still need to invoice correctly and monitor thresholds.

Which VAT Situation Are You In?

Most small businesses and freelancers fall into one of three categories:

1) Exempt Because of the Activity

Certain activities (such as specific health, education, financial or insurance services) are VAT-exempt regardless of turnover.

This exemption depends on what you do, not how much you bill.

2) Exempt Because Your Turnover Is Low (Small-Business Exemption)

If your activity is below €15,000 per year, you may qualify for the small-business VAT exemption.

Under this regime:

- You do not charge VAT on Portuguese-taxable invoices

- You cannot deduct VAT on expenses

This exemption must be monitored carefully as revenue grows.

Important: Only Portuguese tax residents can benefit from this exemption.

3) Normal VAT Regime

If you are not exempt — or you exceed the exemption limits — you enter the normal VAT regime.

Under this regime:

- You add VAT to applicable invoices

- You submit periodic VAT returns

- You may deduct VAT on eligible business costs

When Do You Lose the Small-Business Exemption?

If you are under the small-business exemption, two thresholds matter when invoicing Portuguese clients:

If you exceed €15,000 during the previous calendar year

You typically transition to the normal regime from 1 January of the following year.

If you exceed €18,750 during the current calendar year

The change becomes immediate and the invoice that crosses €18,750 should already include VAT.

If VAT was not charged when required, it does not disappear — it becomes your cost.

Practical check:

If you are under the small-business exemption, review the following monthly:

- Are you approaching €15,000 in annual revenue?

- Could your revenue exceed €18,750 during the current year?

VAT costs can compound very quickly and ruin your business’ profitability.

What If Your Clients Are Outside Portugal?

For service providers:

- If you invoice Portuguese clients, Portuguese VAT usually applies

- unless you are exempt

- If you invoice a business client established in another country, you will often not charge Portuguese VAT

- but the invoice must be issued with the correct VAT treatment

- If you invoice a consumer in another country, Portuguese VAT usually applies

- unless you are exempt

Some freelancers assume that being under the small-business exemption means “VAT doesn’t apply to me”, but that is not accurate when you invoice international clients.

The exemption mainly affects whether you charge VAT on services taxable in Portugal and whether you can deduct VAT on expenses. It does not remove the obligation to apply international VAT rules correctly.

Even if you do not charge VAT, your invoices still need to reflect the correct treatment depending on the client.

Practical check:

Before issuing invoices to foreign clients, confirm:

- Is the client a business or a consumer?

- If it is a business, is the VAT number valid (for EU clients)?

- Does the invoice reflect the correct VAT treatment (for example, reverse charge or outside the scope of Portuguese VAT)?

A Practical Example on the small business exemption

You are a consultant based in Portugal and your total revenue comes from:

- €12,000 invoiced to Portuguese clients

- €40,000 invoiced to EU business clients

Total revenue: €52,000.

However, VAT thresholds focus on the portion linked to Portuguese-taxable activity.

If only €12,000 relates to Portuguese clients, you may still qualify for the small-business exemption — even though your total revenue is way higher.

Two freelancers can both earn €52,000:

- One invoices mainly Portuguese clients — will likely be charging VAT.

- One invoices mainly EU companies — may remain exempt of VAT.

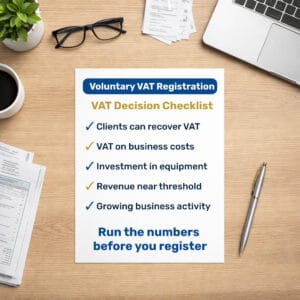

What Changes When You Enter the Normal VAT Regime?

Once in the normal regime:

- You add VAT to your pricing

- You manage VAT reporting deadlines

- You may deduct VAT on business expenses

This changes how you manage cash flow and how you position your pricing.

For some businesses with meaningful expenses, entering the Normal VAT regime can actually improve cost efficiency. For others, it increases pricing pressure and may actually reduce profits.

Important:

Before entering the normal VAT regime you should ask yourself:

- Are you ready to take on the additional admin requirements of becoming VAT-registered?

- different invoicing requirements and VAT reporting deadlines

- Will my pricing still work after adding VAT?

- Business clients can usually recover VAT, but consumers cannot

Your answer may influence how close you want your revenue to get to the VAT exemption thresholds during the year.

Common VAT Misunderstandings

- Assuming “I’m exempt” means VAT is irrelevant

- Exemption affects charging VAT — not invoicing obligations or monitoring

- Missing the €18,750 trigger

- Once crossed, VAT applies immediately

- Treating all revenue the same

- Portuguese clients and foreign business clients may affect VAT differently

These errors often come to light when your VAT regime is reviewed, and correcting them can significantly affect the taxes you pay and your overall profitability.

Final Thought

When monitored regularly, VAT is manageable. When it is ignored, it becomes reactive and expensive.

If your revenue is increasing, your client base is international, or you are unsure how close you are to the threshold, close monitoring usually prevents costly corrections later.